The Importance of Umbrella Insurance in 2024

Personal Umbrella Insurance

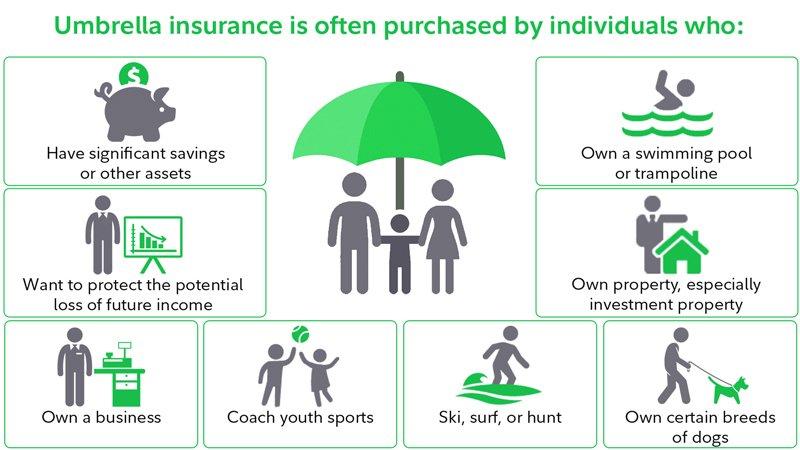

What is Personal Umbrella Insurance

Personal Umbrella insurance provides additional coverage or “excess liability” above the limits of your basic policies. It is designed to provide coverage after your homeowners, renters, auto, and boat insurance policy limits are exhausted. It can also provide coverage for claims that may be excluded by other liability policies.

What does Personal Umbrella Insurance Cover?

It can protect you from bodily injury liability claims such as those sustained in a serious car accident where you’re at fault, or a guest in your home falls, or a neighbor’s child falls while playing in your yard.

It can protect you from property damage claims covering the cost of damage or loss to another person’s property such as damage to vehicles or other property due to an accident where you’re at fault.

They can help cover legal fees in certain lawsuits, such as slander or libel, or if you are sued for false arrest, detention, or imprisonment, malicious prosecution, or shock/mental anguish.

If you are an owner of rental units*, a personal umbrella policy can help protect against liability that you may face as a landlord, such as someone is suing for damages after tripping over a crack in the sidewalk of your rental property or a third party sues you for damages that your tenants cause.

*NOTE: If you run your rental property under a separate business or LLC, your personal umbrella policy (attached to your home or auto insurance, for example) may not be applicable. Please contact us at 480-348-2200 for possible options available to you.

What does Personal Umbrella Insurance Not Cover?

A Personal Umbrella Policy will not cover your injuries or damage to your personal property. It will not cover a criminal or intentional action causing damage to someone else, or any liability you assume under a contract.

How does Personal Umbrella Insurance Work?

A Personal Umbrella Policy kicks in after your basic liability limits have been exhausted or the claim is excluded from the basic liability coverage.

If you are found liable for a claim, your insurance company may pay the settlement amount up to your coverage limits. If a settlement amount exceeds your coverage limits, you are responsible for paying the remaining amount. A Personal Umbrella Policy could pay the remaining settlement amount up to the amount of its policy limits.

Example: If you’re held liable for a car accident and the injuries cost equals $500,000. Your bodily insurance liability on your auto insurance is only $300,000 so your auto insurance will pay the $300,000. You still owe $200,000. A Personal Umbrella Policy would cover the amount above what your auto insurance would pay, up to the limit of the Personal Umbrella Policy.

Why you should have Personal Umbrella Insurance.

Personal Umbrellas policies can provide additional protection for your assets from an unforeseen event or mistake:

-

-

-

- If you are sued and found liable and need to pay damages.

- If you’re sued, all of your assets are exposed. This includes your house, car, any investments and retirement accounts, your checking and savings accounts, and even your future income.

- If you are sued and need to pay for your legal defense – even if the result is that you are not found to be responsible – you should have a Personal Umbrella Policy.

-

-

How much does a Personal Umbrella Insurance Policy Cost?

Personal Umbrella Policies are amazingly affordable. A policy that costs a couple of hundred dollars could give you $1 million coverage. Higher coverage limits would cost more.

How much coverage do I need?

Ask yourself some basic questions when choosing your coverage limits:

-

-

-

- What are your possible risks?

- What risks do you have as a homeowner or renter?

- Could your work commute or driving patterns increase your risk and be a cause for concern?

- Do you have any potentially dangerous activities you participate in that could put those around you at risk?

- What is the value of your assets at risk?

- This would include properties, possessions, stocks, bonds, savings, and retirement funds.

- The more assets you have to protect, the higher the umbrella policy limit you should consider.

- What is the potential loss of your future income?

- When you review your future income, consider your earning potential.

- Liability lawsuits can result in the loss of both current assets and future income. So, even if you have only a few assets now to protect, you may want to consider the long-term consequences of a serious claim.

- If you’re a medical student and you’re on a course for a high-paying career, you could be involved in a lawsuit that can target money you haven’t earned yet.

- What are your possible risks?

-

-

Give us a call at 480-348-2200 and get a free umbrella insurance quote powered by Inszone Insurance Services! We can help you identify your specific risk factors and learn more about how to protect your current and future assets. We will comparison shop policies from various insurance companies, and help you find a policy to specifically meet your needs and budget.